A buzzy startup offering financial infrastructure to crypto companies has found itself bankrupt primarily because it can’t gain access to a physical crypto wallet with $38.9 million in it. The company also did not write down recovery phrases, locking itself out of the wallet forever in something it has called “The Wallet Event” to a bankruptcy judge.

Prime Trust pitches itself as a crypto fintech company designed to help other startups offer crypto retirement plans, know-your-customer interfaces, ensure liquidity, and a host of other services. It says it can help companies build crypto exchanges, payment platforms, and create stablecoins for its clients. The company has not had a good few months . In June, the state of Nevada filed to seize control of the company because it was near insolvency. It was then ordered to cease all operations by a federal judge because it allegedly used customers’ money to cover withdrawal requests from other companies.

The company filed for bankruptcy, and, according to a filing by its interim CEO , which you really should read in full, the company offers an “all-in-one solution for customers that remains unmatched in the marketplace.” A large problem, among more run-of-the-mill crypto economy problems such as “lack of operational and spending oversight” and “regulatory issues,” is the fact that it lost access to a physical wallet it was keeping a tens of millions of dollars in, and cannot get back into it.

“In March of 2018, the Company created cold-storage wallets for purposes of maintaining cryptocurrency assets that included ETH, BTC, and ERC-20 compliant cryptocurrencies,” the company wrote in its filing. It called one of these wallets the “98f Wallet,” because its address ended in “98f.”

Image: Court records

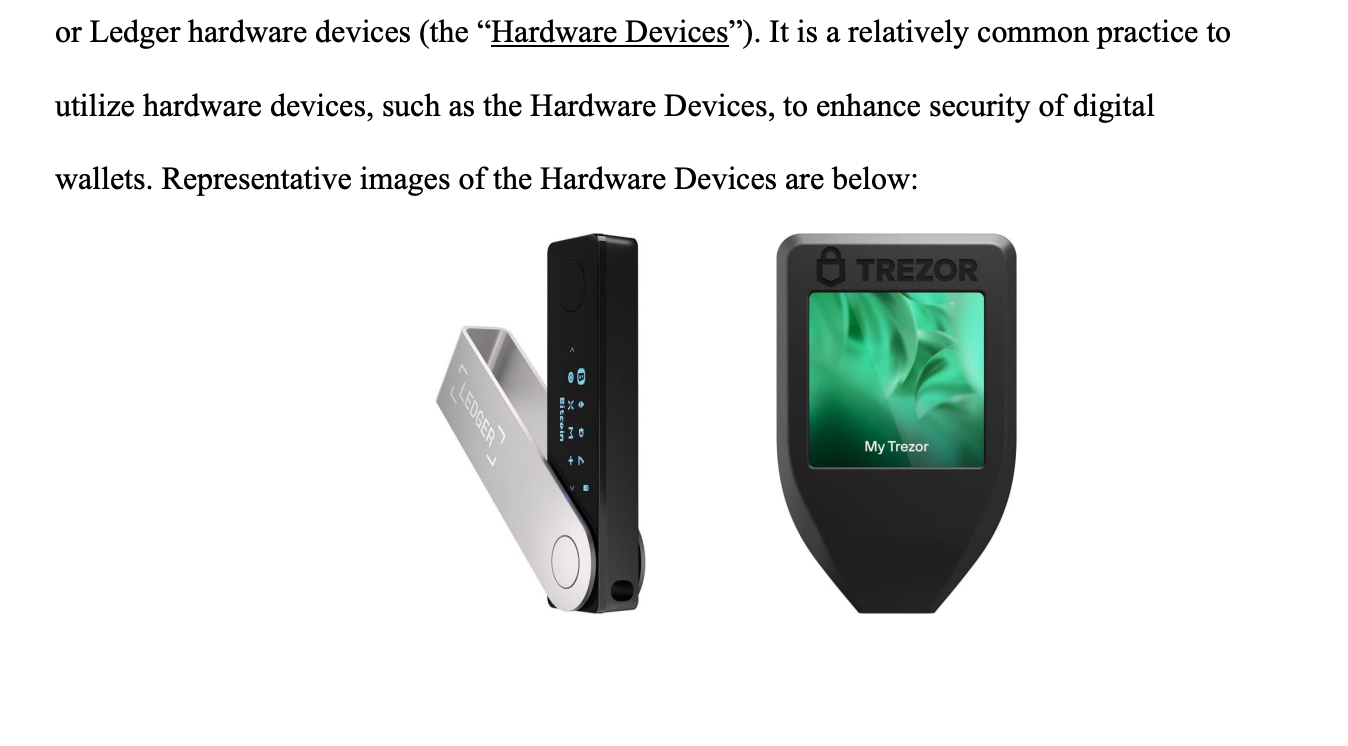

“To enhance security, the Company set up the 98f Wallet so that those who can ‘sign’ (i.e., approve) transactions would need to be in physical possession of hand-held Trezor or Ledger hardware devices,” the filing says.

The filing then states that, if the wallet is lost, most users create “seed phrases” that serve as backup codes that allow people to get into the wallet virtually: “Many users store seed phrases on hard copies of handwritten paper, images, and pictures. If a user loses both the hardware device and the seed phrases, it is virtually impossible for that user to regain access to the digital wallet.”

You can probably see where this is going.

Rather than write down the seed phrases, Prime Trust opted to laser etch them into a piece of steel called “Cryptosteel Hardware,” which are called “Wallet Access Devices” in the court filings, and which look like this:

Image: Court records

According to the filing, it lost these devices, which is why it can’t get back into the wallet.

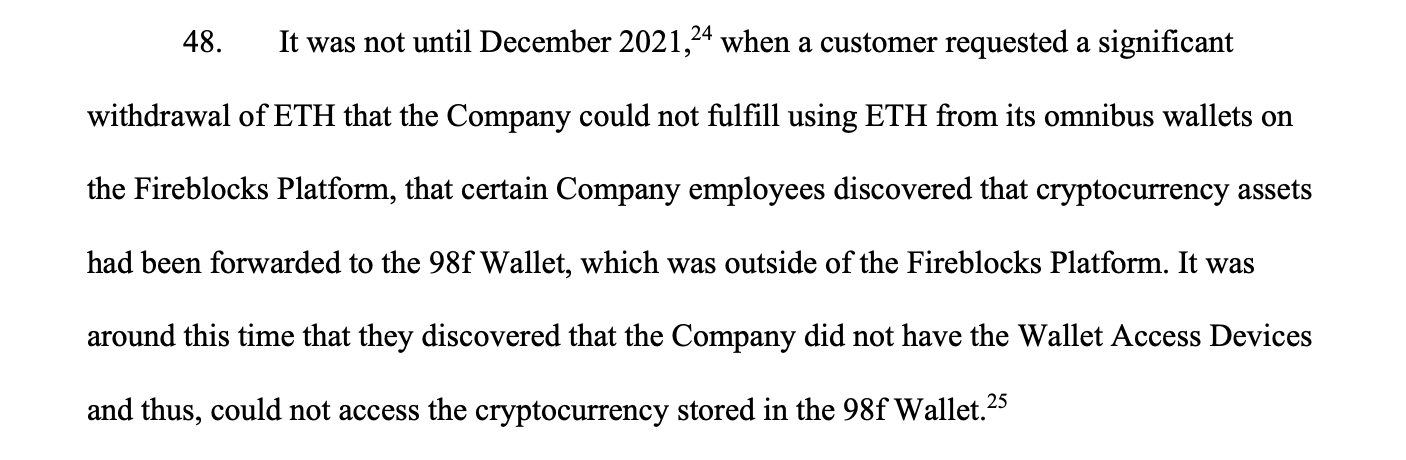

For several years, the company then took customer deposits into this address, to the tune of tens of millions of dollars. In December, 2021, “when a customer requested a significant withdrawal of ETH that the company could not fulfill [from other wallets,]” it went to withdraw it from this hardware wallet. “It was around this time that they discovered that the Company did not have the Wallet Access Devices and thus, could not access the cryptocurrency stored in the 98f Wallet.”

Image: Court records

The company then, for several months, had to “use $76,367,247.90 in the aggregate to purchase ETH to fund customer withdrawals.” The money stuck in the wallet is currently worth $38.9 million as of August 22, it claimed. It is worth mentioning that the company did not tell regulators or customers about this issue for months after it discovered the problem.

All of the many ways this went wrong was broken down in detail in a great thread by Patrick McKenzie of Stripe .

The company has still not solved this issue: “The Company remains unable to access the 98f Wallet,” it wrote. “The investigation continues.”

Prime Trust swears in its filing that this was an “aberrant” event and “extremely unlikely to occur again.”